Problem:

There are over 70 million people in the U.S. alone who are classified as “underserved” by traditional financial institutions including approximately 20 million people with no bank account and millennials who are abandoning traditional banks in favor of on-line and mobile banking and payment services delivered through their smart-phones.

The traditional approach to designing breakthrough programs for these individuals, from purchases made with a Visa or MasterCard, wire transfers, peer to peer remittance, ATM access, payroll, foreign exchange (FX) transactions and check cashing, is highly restrictive, costly and often fails when moving from idea to execution. This has led to the creation of a product-market gap for both the businesses looking to extend their brand into payments and for those consumers who are underserved by the traditional products in the market today. ECHO bridges this gap by designing highly customized, low cost, profitable and fully functional products for their clients.

Solution:

Unlike our competitors, ECHO directly addresses this product-market gap by providing highly customized payment programs designed for Businesses and Consumers and then seamlessly integrating those programs into their partners brand and operations to reduce costs, increase revenue and extend brand reach creating either a physical card, smartphone/ tablet app or as a virtual payment card.

Business Summary:

As reported by Inc. Magazine, “Long seen as a highly technical, highly regulated industry dominated by giant banks that resist disruption… finance is now riding an entrepreneurial wave. Demand for upstart services is strong, piqued by widespread frustration with big banks…” ECHO seeks to disrupt this market dynamic and leverage the inability of market incumbents to drive innovation or support customization to create sustainable profit through the issuance of customized physical, virtual and mobile payment and remittance (money send) products that enable businesses to better serve their customers and allowing individuals to better serve their personal payment needs.

Business Model:

ECHO’s main sources of revenue are: (1) monthly fees charged to card holders ranging from $3.95 to $9.95; (2) interchange paid by merchants approximating 1.5% of gross transaction volume; (3) transaction fees of $1.00 to $2.50; (4) implementation fees generated through customized program design for business clients. Additional sources of income include performance bonuses paid by Visa.

Management:

ECHO’s unique management composition consists of globally experienced banking, payment, technology, network, processor, card-manufacturing and sales experts.

Target Market / Size: USA:

Fintech, brick and mortar, and software-as-a-solution companies seeking to participate and profit from the nearly $65 billion payment market driven by the established and growing financial needs of the Unbanked (20MM); Underserved (70MM); Small and Medium Sized Enterprises (4MM); and Millennials (77MM).

Customers – Current / Potential:

Current customers under contract : $52M top line revenue over 5 years

Near term Pipeline customer potential: $125M top line revenue over 5 years

RFP response with incumbent provider: $300M top line revenue over 5 years

Sales / Marketing Strategy:

ECHO has four main methods of generating new card programs: (1) a strong business partner referral network which includes card associations, strategic agreements with processors, industry consultants and issuing bank partners (2) providing a distribution channel for other Fintech and SaaS companies looking for cost effective and profitable entries into the Payment Ecosystem. (3) sales through partner’s distribution channels such as lenders, check cashers, payroll providers, health care networks, and (4) direct-to-consumer programs through online sales.

Competitors:

ECHO’s competitors include Simple, Greendot, NetSpend and Account Now. Simple was recently acquired by BBVA for $117MM, giving them a valuation of over $1,000 per account. NetSpend and Greendot valuations are closer to $600 per active account.

Competitive Advantages: Specific advantages include:(1) ECHO’s unique management composition; (2) ECHO’s proprietary middleware that allows ECHO to work around legacy systems and processes to integrate new features and programs quickly and effectively (3) Product Innovation including mobile applications for loading checks and global remittance capabilities; and (4) ECHO’s low cost infrastructure including high quality offshore IT development.

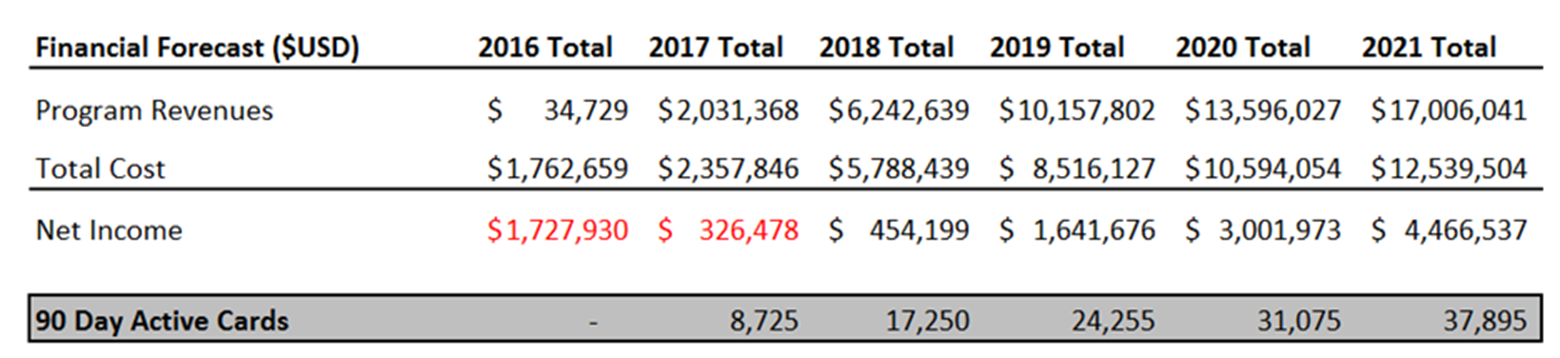

Worst Case Financials

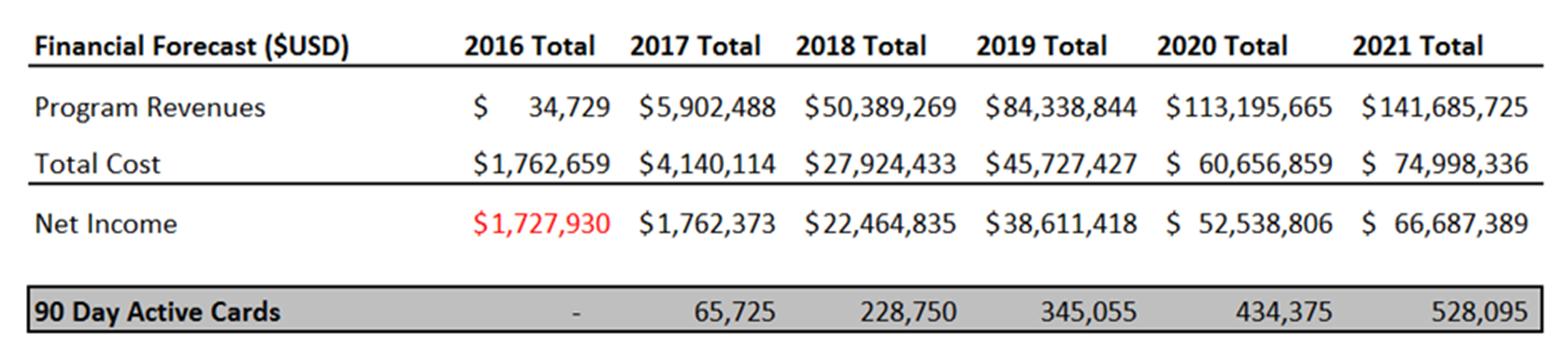

Expected Case Financials

Management Bios:

Ronald Ingram is the founder of ECHO Payment Systems Inc.

Since the early 1990s, Mr. Ingram has been inventing ground-breaking technology to improve accessibility and security of fintech services for those who are underserved by traditional banks. During this time, Ron Ingram founded the company that has evolved into Beanstream Internet Commerce, Inc., one of the first providers of authentication and electronic payment processing solutions. Mr. Ingram raised Bean stream’s first venture capital funding, launching the fledgling company on its path to success. Beanstream is now the largest of its competitors, processing over $30 billion annually for 18,000 businesses, which now include eBay and PayPal.

After Beanstream, Mr. Ingram spent four years creating ground-breaking financial products for DFC Global. During this time, Mr. Ingram founded and managed the Nextwave Card Corporation where he launched next generation products, such as Nextwave® Titanium MasterCard, CreditLink, and iLoan product lines, and contributed millions to the bottom lines of all involved partners. Nextwave® became the template for future U.S., Canadian, and UK programs and, to date, is the most successful program in its category.

In 2005, Gerson Lehrman Group (“GLG”) discovered Mr. Ingram due to industry buzz over Mr. Ingram’s fintech product announcements. GLG, headquartered in New York, is the world’s largest membership-based network of more than 425,000 thought leaders and practitioner consultants whose subject matter specialists, recognized for their outstanding achievements, offer expert judgments, opinions, and advice to GLG’s Fortune 500 client companies.

As a GLG Leader in alternative financial services, Mr. Ingram has influenced the multi-billion-dollar decisions of private equity funds, venture capital firms, nine of the top ten investment banks and “Big 5” consulting firms.

Since 2003, Mr. Ingram has managed programs that have issued more than 6 million general purpose reloadable cards in partnership with Visa, MasterCard, Galileo, Peoples Trust and Metabank among several other companies.

Ronald Ingram was granted “Extraordinary Alien” status by the United States Citizenship and Immigration Service (USCIS) in 2017 and lives in Henderson, Nevada with his wife, Kirsten, of 26 years and two rescued dogs. He can be followed @imaginician on Twitter.

Michael Devlin is the President and a co-founder of ECHO Payment Systems Inc.

Mr. Devlin is an accomplished and award winning executive in payments with international experience across North America, the United Arab Emirates (UAE), India, Pakistan, Europe, and Australia. His global perspective in payments drives a unique perspective on the history and evolution of payments and payment trends including those in the fintech sphere. Mr. Devlin has leveraged this perspective to drive many industry “first thoughts” in his career including: the first launch of contactless payments in Canada with Citibank and MasterCard; managing some of the largest MasterCard co-brand card portfolios including the Shell, ExxonMobile, Reliance Retail India and PetroCanada; initiating the largest mobile payment test in India’s history with MasterCard including securing the largest exclusive Visa Debit issuance deal with Citibank India;, and securing the largest addition of Visa Branded network ATM’s in Canada.

Most recently, prior to co-founding ECHO, Mr. Devlin was the Vice President Payments with Jamieson Bank responsible for the design, development and launch of a payment business including securing the approval of the Canadian Federal Banking Regulator (OSFI) to launch the first new line of business for this bank since its inception. When Jamieson Bank was acquired by Associated Foreign Exchange (AFEX), the largest non-bank provider of Foreign Exchange globally, with an annual turn of more than $15B in currency, AFEX retained Mr. Devlin to launch a global payment business for their company. Mr. Devlin successfully developed, staffed and launched this endeavour for AFEX in the United Kingdom prior to his acceptance of the role of President at ECHO Payment Systems

Mr. Devlin attributes his success to his life-long passion for creating meaningful and lasting personal connections that enable mutual success. He embodies this belief in his personal life through a strong commitment to children’s and charitable causes and has been recognized for this work in his selection and acceptance of the of the Laurier MBA Alumni Award for Community Leadership recognizing his exceptional generosity and outstanding charitable responsibility, including encouraging others to take philanthropic leadership roles in the community.

Michael currently resides in Toronto, Canada with his wife, Nadine Cannata, and their three children, Matthew, Lauren and Caleb.

Jay Fischbach is the Vice President, Product of ECHO Payment Systems Inc.

Mr. Fischbach has been an executive in the financial services sector for the past twelve years and has worked in Finance/Technology for the past twenty years. He has an excellent grasp of the key factors that are critical for the success of a financial technology organization, which are solid financial and operational knowledge, clear understanding of operational efficiencies and how to manage and successfully mentor staff.

Having spent half his career in smaller, entrepreneurial organizations and the other half working worldwide for one of Canada’s largest organizations, he has gained valuable knowledge of various roles within Capital Markets. From Finance to Operations to Compliance, Sales and Technology, he has worked in or closely with all departments and can easily transition between these in order to develop and implement key growth initiatives. Further, having spent time working within various Capital Market frameworks and with multiple regulators, he understands how to prioritize programs to ensure his organization always remains compliant.

With respect to Operational Management, Mr. Fischbach created and implemented key programs both within RBC Dexia and while operating as the COO of Jameson Bank. These were used to measure and manage staff, departments and clients. While at Jameson Bank he implemented the Process Improvement Program which resulted in a year over year 32% cost reduction. While at RBC Dexia he was responsible for the development and oversight of the Global Operational Excellence program, Network Management for the America’s and was the program lead on the €130M Custody Platform consolidation project. Throughout his career, he has had a unique ability to grasp very complex issues and break them down to both explain and optimize.

In his prior role at AFEX as Country Head, Canada, Mr. Fischbach led the sales team across 6 cities, opened multiple offices and drove increased revenues year over year. He was also responsible for the acquisition and integration of multiple businesses within the region. Fischbach played a key role in the broader AFEX organization as member of the global executive management team and was called on to lead various program strategy initiatives.

Throughout his twenty years in business, he believes that his greatest achievements have always been the development of high-performing teams, central to his core belief that, “No one can accomplish success on their own. They need great people around them who want to exceed expectations.”

Jay lives in Toronto, Canada with his wife and two children. Jay is very active father, golfer and runner and is preparing to run his first Marathon this summer.

RSVP deadline is past